Pursuant to the first subparagraph of Article 2433-bis of Italian Civil Code (hereinafter “C.C.”), distribution of interim dividends is only allowed in companies “obliged by law to submit their financial statements to a legal auditing, in accordance with the arrangements established by special laws for public-interest entities”. Banking institutions, insurance institutions and listed companies currently constitute the so-called public-interest entities (PIEs, definition amended by Legislative Decree no 135 of 2016).

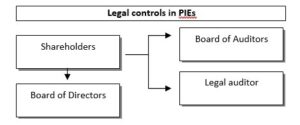

The main feature of the auditing of PIE is that the Board of Auditors (Collegio Sindacale) cannot carry out legal auditing of accounts, but it can exercise its supervisory role only on the company management (Article 16, subparagraph 2, of Legislative Decree no. 39 of 2010). The legal auditing, instead, must be necessarily carried out by an external legal auditor (an independent auditor, revisore or a legal auditing company, società di revisione), that has to fulfil a series of independence requirements. This means that in PIEs the Control Body must be composed of two organs, the Board of Auditors and an independent auditor or an external auditing company, as shown in the table below:

Provided that Art. 2433-bis of C.C. in order to distribute interim dividends requires that companies shall be obliged by law (it’s an objective requirement) to submit their statements to a legal auditing as for PIEs, it is necessary to verify whether a limited company having a corporate structure abstractly comparable to that requested for a public-interest entity can be considered obliged to adopt a Control Body similar to that of PIEs (i.e. composed by the Board of Auditors and by an external legal auditing company or independent auditor registered with the Registry of Legal Auditors of the Ministry of Economy and Finances) or if this would be just an optional scheme.The issue is quite complex because the reference rule of law (Article 2477 of C.C.) has been frequently amended over the last five years, leading to several problems of coordination with other legislative provisions.

The present wording of the Article 2477 establishes that “the appointment of a control body or of a legal auditor (revisore legale) is mandatory where:

- the company is required to draw up consolidated accounts;

- the company controls an entity subject to legal auditing of its accounts;

- for two consecutive financial years the company exceeded almost two of the limits of Art. 2435 bis”, i.e.:

- Total assets: Euro 4.400.000

- Total revenue: Euro 8.800.000

- Average number of employees during the financial year: 50.

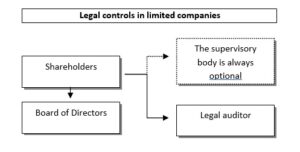

Thus, the mentioned Article gives to the shareholders of a limited company the choice to appoint, alternately, a Control Body (Sole Auditor or Board of Auditors) or a legal auditor (revisore legale), which means that the appointment of a Board of Auditors or of a Sole Auditor is purely optional for limited companies and not mandatory, because a limited company that meet the requirements under letters a), b), c) has the choice to appoint only a legal auditor to fulfil the obligations under Article 2477 of C.C. (please see the table below).

Now, considering that for PIEs (that are considered sensitive companies) Article 16 of Legislative Decree no. 39 of 2010 states that the statutory audit cannot be carried out by the Board of Auditors, it does not appear plausible to include a limited company, which is currently not even obliged by law to appoint a Board of Auditors, into the definition of companies entitled to distribute interim dividends pursuant to Art. 2433-bis of C.C., i.e. those “obliged by law to submit their financial statements to a legal auditing, in accordance with the arrangements established by special laws for public-interest entities”. In fact, the arrangements established by special laws for PIEs presume the presence of a Board of Auditors, considering also that in PIEs the Board assumes the role of Internal Control and Audit Committee, whereas in limited companies the Board is purely optional and not mandatory. Then, in my opinion, it does not seem possible to consider a limited company as a company obliged by law to submit its accounts to a legal auditing within the meaning of the first paragraph of Article 2433-bis of C.C, notwithstanding it would have a corporate structure abstractly comparable to that requested for a PIE. Contrary to what happens with PIEs, limited companies are not obliged by-law to appoint a Board of Auditors. Therefore, a limited company does not seem to fulfil the requirements established by the first paragraph of Article 2433-bis of C.C. needed in order to distribute interim dividends, except in the unlikely event where the limited company would be a PIE.

For further details, please contact:

Lawyer Luca Salvi

Phone (+39) 06 97996055